The short answer

Litigation support services are the financial and investigative work counsel engages to build or rebut a case: quantifying economic damages, reconstructing income and fund flows through forensic accounting, tracing assets for enforcement or recovery, and delivering expert testimony that withstands scrutiny under Federal Rule of Evidence 702. They are used from pre-suit through verdict, on both plaintiff and defense sides.

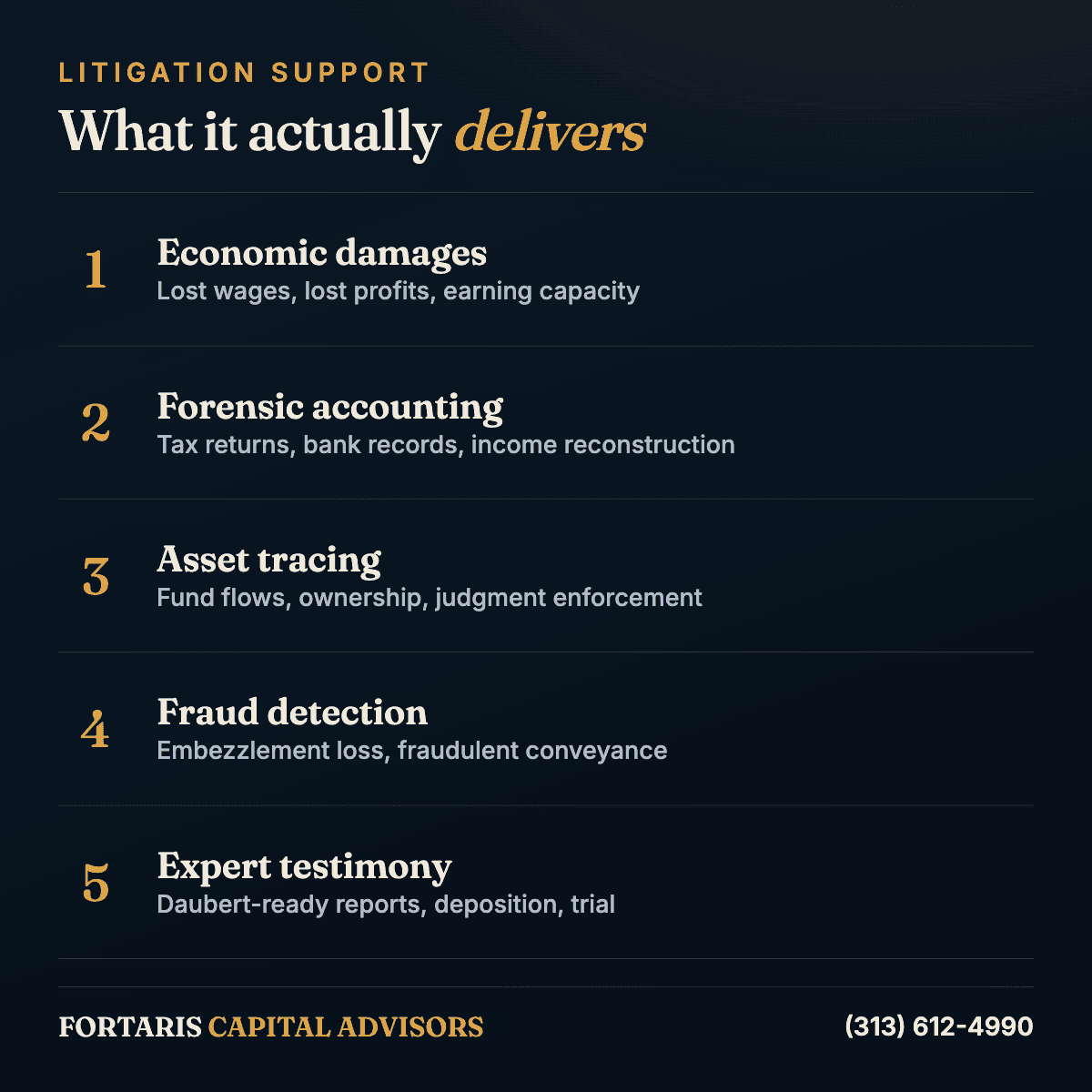

What litigation support services actually cover

The phrase covers more ground than most parties expect. In practice, litigation support is the financial and investigative capability a legal team does not hold in-house: the ability to put a defensible number on a loss, to reconstruct what happened inside a set of financial records, to find what a party would prefer stayed unfound, and then to explain all of it under cross-examination.

It is not a single deliverable. A matter may need a damages model and nothing else. Another may need an asset trace and never see a courtroom. A third needs the full arc — investigation, quantification, report, deposition, testimony. The common thread is that each output has to survive an adversary whose job is to dismantle it.

Fortaris supports both plaintiff- and defense-side engagements across commercial litigation, arbitration, regulatory enforcement, white-collar defense, and bankruptcy and receivership matters.

- Economic damages and financial-loss analysis — lost wages, lost profits, business interruption, diminished earning capacity

- Forensic accounting — tax-return, bank-record, and financial-statement analysis; income reconstruction

- Asset tracing and financial investigations — locating assets, mapping ownership, following fund flows

- Fraud and misrepresentation detection — embezzlement loss, related-party transactions, fraudulent conveyance

- Expert testimony — Daubert-ready reports, deposition, and trial or arbitration testimony

The most expensive mistake is bringing the expert in late

Counsel often engages financial expertise once a damages figure is contested — after the pleadings are set, after discovery has been scoped, sometimes after a deposition has locked in a theory. By then the expert is being asked to defend a position rather than help shape one.

Brought in early, the same work does something more useful: it tells you what the loss actually is before you plead it, identifies the records you need before you serve requests, and surfaces the weaknesses in your own theory while there is still time to adjust. It also frequently narrows the matter. A credible early number can make settlement rational for both sides — or reveal that a claim will not carry the weight being placed on it.

This is the same logic that governs investigative due diligence before a transaction: the value of the work is highest at the point where findings can still change the decision.

Economic damages: the number has to survive cross-examination

Damages quantification is the core of the practice. In personal-injury and wrongful-loss matters, that means past and ongoing lost wages, future earning-capacity assessments across a claimant's work-life horizon, and — the hardest category — income reconstruction for self-employed claimants and closely held businesses whose records are incomplete or contested.

In commercial disputes, it means lost-profit and business-interruption analysis, and economic-damages modeling in contract, shareholder, partnership, and M&A disputes. The technical work is only half of it. The other half is documentation: a number that cannot be traced back through its inputs, assumptions, and method is a number that will not hold.

The discipline that matters here is restraint. An aggressive figure that collapses under scrutiny is worth less than a conservative one that does not move.

Asset tracing: finding what is there, and what was moved

A judgment is not a recovery. Asset tracing is the work of turning one into the other — locating assets, identifying ownership pathways, and following fund flows to support judgment enforcement and post-fraud recovery.

Much of the value sits in what the movement itself reveals. Fraudulent-conveyance analysis and related-party transaction reviews often show assets shifted to relatives, affiliated entities, or trusts in the window before a claim landed. That pattern is frequently more probative than the balance sheet it was designed to protect. This work also supports trustees, receivers, debtors-in-possession, and creditors' committees.

Where funds or ownership cross borders, the analysis compounds — different registries, different disclosure regimes, different evidentiary standards. That terrain is covered in our guide to cross-border fraud investigation, and it draws on the same capability as our investigative services and corporate intelligence practices.

Expert testimony: the bar moved in 2023

Counsel evaluating experts should understand what changed. Effective December 1, 2023, Federal Rule of Evidence 702 was amended to make explicit what many courts had been applying loosely. The proponent must now demonstrate that it is more likely than not that the testimony meets the rule's requirements — a preponderance standard for admissibility, not a question of weight left to the jury.

The amendment also sharpened Rule 702(d): the expert's opinion must reflect a reliable application of the principles and methods to the facts of the case. In plain terms, an expert may no longer stretch a conclusion beyond what the underlying method and data actually support, and courts were specifically cautioned about experts asserting more certainty than a subjective method can carry.

The practical consequence is that methodology and candour are now admissibility issues. This favours experts who document their inputs, state their limits, and decline to overclaim — and it exposes those who treat a report as advocacy. Independence is not a soft virtue here; it is the thing that keeps the opinion in front of the jury.

- The proponent carries a preponderance burden on admissibility — it is not automatically a weight question

- The opinion must reflect a reliable application of the method to these facts, not the method in the abstract

- Overstated certainty is a specific target of the amendment, particularly for subjective methods

- Daubert-ready means the report anticipates the challenge before it is filed

What drives the cost of an engagement

Litigation support is scoped, not priced from a menu, and the drivers are reasonably predictable. The condition of the records matters most: reconstructing income for a cash-intensive business with incomplete books is a different exercise from analysing clean audited statements. Scope matters next — a discrete lost-wage calculation is not a multi-entity fraud trace.

Beyond that: the number of jurisdictions involved, the volume of financial data, whether assets must be traced through intermediaries, the compression of the litigation timeline, and whether the engagement ends at a report or continues through deposition and trial testimony. Testimony carries its own preparation burden and should be scoped as its own phase.

Any firm quoting a confident figure before seeing the records is guessing. The honest answer to “what will this cost” begins with a look at what you actually have.

How to choose a litigation support firm

The market ranges from large advisory firms to solo testifying experts, and the right choice depends on the matter. A few questions separate them quickly.

Ask who will actually do the work and who will sign the report — at many firms these are different people, and the second one meets you at the pitch. Ask what the credentials are: CPA and forensic-accounting depth for damages, ACFE Certified Fraud Examiner methodology where fraud is alleged, and genuine financial-investigative experience where assets have to be found rather than counted. Ask about testimony history, including matters where the opinion was challenged.

Then ask the uncomfortable one: what would make you decline to give the opinion we want? An expert who cannot answer that is a liability under the amended Rule 702. Fortaris's litigation support practice is Managing-Director-led and built on CPA, forensic-accounting, and federal financial-investigative experience — delivered as independent conclusions, which is the only kind that helps law firms when the report is tested.

Key takeaways

- Litigation support spans economic damages, forensic accounting, asset tracing, fraud detection, and expert testimony — used pre-suit through verdict, plaintiff- and defense-side.

- Engaging the expert early shapes the damages theory and discovery plan; engaging late reduces the expert to defending a position already taken.

- A damages figure is only as good as its documentation — a number that cannot be traced through its inputs and assumptions will not survive cross-examination.

- Asset tracing turns a judgment into a recovery, and the movement of assets is often more probative than the assets themselves.

- The December 2023 amendment to Rule 702 put a preponderance burden on the proponent and requires the opinion to reflect a reliable application of the method — overclaiming is now an admissibility risk.

Frequently asked

What are litigation support services?

They are the financial and investigative services counsel engages to build or rebut a case: quantifying economic damages, forensic accounting and income reconstruction, tracing assets for enforcement or recovery, detecting fraud and misrepresentation, and providing expert reports and testimony. They are used from pre-suit through verdict, on both plaintiff and defense sides.

How is litigation support different from a testifying expert?

A testifying expert delivers an opinion and defends it. Litigation support is broader: it includes the investigative and forensic work that produces the underlying facts — locating assets, reconstructing income, analysing records — which may or may not end in testimony. Many engagements never reach a courtroom; some are consulting-only and never disclosed.

When should counsel engage a litigation support firm?

As early as the damages theory is being formed — ideally pre-suit. Early involvement establishes what the loss actually is before it is pleaded, identifies the records to request in discovery, and surfaces weaknesses while there is still time to address them. Late engagement narrows the expert's role to defending positions already locked in.

What changed with Federal Rule of Evidence 702 in 2023?

Effective December 1, 2023, Rule 702 was amended to clarify that the proponent must demonstrate by a preponderance of the evidence that the testimony meets the rule's requirements, rather than treating the sufficiency of the expert's basis as a question of weight. It also emphasises that the opinion must reflect a reliable application of the principles and methods to the facts, discouraging experts from asserting more certainty than their method supports.

What does 'Daubert-ready' actually mean?

That the report is built anticipating a challenge to its admissibility: the method is established and stated, the inputs and assumptions are documented and traceable, the application to these specific facts is explained, limitations are disclosed, and the conclusion does not exceed what the data and method support.

Can you trace assets that have been moved to family members or other entities?

That pattern is a routine focus of the work. Fraudulent-conveyance analysis and related-party transaction reviews examine transfers made in the period before or after a claim arose. The timing and structure of the movement is often more evidentially valuable than the assets themselves.

What does litigation support cost?

It is scoped per matter. The main drivers are the condition and volume of the financial records, the breadth of the question, the number of jurisdictions and entities involved, the litigation timeline, and whether the engagement ends at a report or continues through deposition and trial. A firm quoting a confident figure before reviewing the records is estimating without a basis.

Do you work for both plaintiffs and defendants?

Yes. The analysis does not change with the side of the caption — the method, documentation, and willingness to state limits are the same. An expert whose conclusions track whoever retained them is the expert most exposed under the amended Rule 702.

How do I choose between a large advisory firm and a boutique?

Ask who performs the work and who signs the report, what the credentials are (CPA and forensic-accounting depth for damages; ACFE Certified Fraud Examiner methodology where fraud is alleged; real investigative experience where assets must be found), and what the testimony record looks like — including challenged matters. Large firms offer scale; senior-led boutiques offer the person you met doing the actual work.

Sources & further reading

- Federal Rule of Evidence 702 (as amended Dec. 1, 2023) — Sets the admissibility standard for expert testimony: the proponent must demonstrate the requirements are met by a preponderance, and the opinion must reflect a reliable application of the principles and methods to the facts.

- Daubert v. Merrell Dow Pharmaceuticals, Inc., 509 U.S. 579 (1993) — Established the trial court's gatekeeping role over the reliability and relevance of expert scientific testimony; the framework Rule 702 codifies.

- Federal Rule of Civil Procedure 26(a)(2) — Governs disclosure of testifying experts and the required contents of the written report, including the basis and reasons for the opinions.

- Association of Certified Fraud Examiners (ACFE) — Source of the Certified Fraud Examiner credential and methodology applied in fraud, embezzlement, and misrepresentation matters.

- AICPA Forensic & Valuation Services — Professional standards and practice aids governing forensic accounting and economic-damages engagements performed by CPAs.